Over 38 million Nigerians use mobile money services today — and a major ownership shift is about to change who controls one of the biggest platforms serving them. MTN Nigeria shareholders approved the MTN Nigeria MoMo PSB stake sale 2026 on April 30, 2026. The deal is worth approximately N152 billion and hands a 60% stake in MoMo Payment Service Bank (PSB) to MTN’s South African parent company. If you use MoMo, or if you care about Nigeria’s fintech future, this deal affects you directly.

Key Takeaways 📌

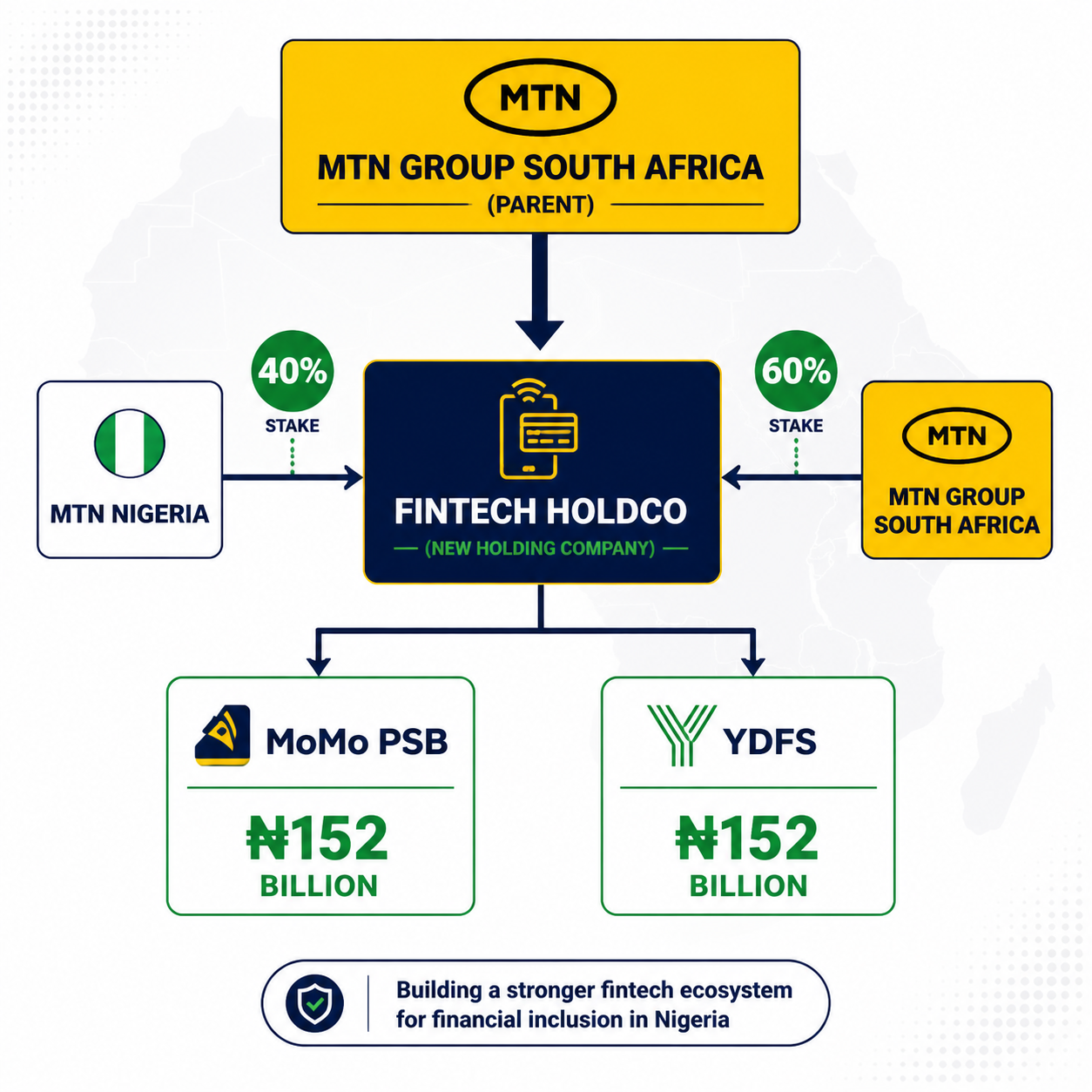

- MTN Nigeria is selling a 60% stake in MoMo PSB and Yellow Digital Financial Services (YDFS) to MTN Group for about N95.5 billion

- Total capital injection into the two fintech units is approximately N152 billion

- MTN Nigeria keeps 40% — it’s not walking away from fintech, just reducing its direct burden

- A new Fintech HoldCo will be registered with the Central Bank of Nigeria to hold both stakes

- Completion is expected by December 31, 2026, pending regulatory approval

What Actually Happened With the MTN Nigeria MoMo PSB Stake Sale 2026

MTN Group announced the deal on April 29, 2026. The announcement came in an explanatory note filed with the Nigerian Exchange (NGX). This was done ahead of MTN Nigeria’s Annual General Meeting the next day.

Shareholders voted and approved the deal on April 30, 2026.

Here’s the simple breakdown of what was agreed:

| Item | Detail |

|---|---|

| Stake being sold | 60% of MoMo PSB + YDFS |

| Buyer | MTN Group (South Africa) |

| MTN Nigeria retains | 40% stake |

| Deal value (stake) | ~N95.5 billion |

| Total capital injection | ~N152 billion |

| Expected completion | By December 31, 2026 |

| Regulatory body | Central Bank of Nigeria |

The deal has two phases. First, MTN Group Fintech acquires its 60% position using a mix of new shares and existing shares. Second, a brand-new Holding Company — called Fintech HoldCo — is created. Both MTN Group and MTN Nigeria then move their stakes into this new entity. The HoldCo will be registered with the Central Bank of Nigeria.

This is technically an intra-group restructuring. The money stays within the MTN family. But the power and control shift significantly toward the parent company.

💡 Quick fact: MTN Nigeria had actually bought the remaining 7.17% minority stake in MoMo PSB in May 2024 for N6.95 billion. That made it 100% owner. Now, just two years later, it’s selling 60% of that back up to its parent.

Why MTN Nigeria Is Doing This Now

The honest answer? MoMo PSB was losing money — a lot of it.

MTN Nigeria recorded a N62.56 billion impairment on its fintech investments in 2025. An impairment means the company officially admitted those assets were worth less than what it paid for them. That’s a significant financial hit.

Running a payment service bank in Nigeria is expensive. You need agents, infrastructure, regulatory compliance, and constant capital. MTN Nigeria was carrying all of that weight alone.

The MTN Nigeria MoMo PSB stake sale 2026 is partly about offloading that financial pressure. By bringing MTN Group in as the majority owner, the parent company now carries the bigger share of costs and risks.

MTN Nigeria can then focus on defending its core telecom business. That business is also under pressure from rising competition, naira devaluation, and high operating costs.

This move also fits into MTN Group’s bigger plan called “Ambition 2030.” That strategy aims to make MTN Group Africa’s leading platform for connectivity, fintech, and digital infrastructure. Centralising fintech operations under one roof — across multiple African countries — is a key part of that plan.

What This Means for Nigeria’s Fintech Landscape

Nigeria’s mobile money and digital payments space is one of the most competitive in Africa. MoMo PSB doesn’t operate in a quiet market. It competes directly with:

- 🟢 OPay — backed by Chinese investors, massive agent network

- 🔵 PalmPay — fast-growing, strong merchant presence

- 🟡 Kuda Bank — digital-first, popular with younger users

- 🟠 Moniepoint — strong SME and agent banking play

MoMo PSB has struggled to keep up with these rivals despite MTN’s massive subscriber base. The restructuring is meant to fix that.

With MTN Group now holding 60%, MoMo PSB gets:

✅ More capital from a larger, better-funded parent

✅ Strategic direction aligned with pan-African fintech goals

✅ Reduced dependency on MTN Nigeria’s own balance sheet

✅ Potential tech and operational support from other MTN markets

For Nigeria’s broader fintech ecosystem, this signals something important. Even telecom giants with millions of subscribers find it hard to run profitable mobile money operations. It takes focused capital, strategy, and patience.

The latest trends in digital wallets and mobile payments show that mobile money is still growing fast globally. But competition is fierce, and only well-funded players survive long-term.

What It Means for Everyday MoMo Users in Nigeria

Let’s be direct: your MoMo account isn’t going anywhere.

This is a corporate restructuring. It changes who owns and controls MoMo PSB behind the scenes. It doesn’t change the app, the USSD code, or your wallet balance.

Here’s a realistic Nigerian use case:

Amaka in Aba uses MoMo PSB to receive payments from her fabric customers. She doesn’t have a bank account. For her, MoMo is her bank. This deal, if it brings more capital and better service, could mean faster transactions, more agents near her, and fewer downtime issues.

But that’s the best-case scenario. It’s not guaranteed.

What could realistically improve:

- More investment in MoMo’s agent network

- Better app stability and uptime

- Possible new features aligned with MTN Group’s pan-African fintech tools

What might not change quickly:

- Day-to-day service quality (that depends on execution, not just ownership)

- Competition from OPay and PalmPay, which are already deeply embedded

- Nigeria’s broader infrastructure challenges — power, internet reliability, device access

The deal still needs regulatory approval from Nigerian authorities. Until that comes through, nothing officially changes. Completion is targeted for December 31, 2026.

The Reality Check: Limitations and Local Challenges

It’s easy to read a headline like “N152 billion fintech deal” and assume everything will improve overnight. It won’t.

Here are the honest limitations to consider:

1. Regulatory approval is not guaranteed

The Central Bank of Nigeria must approve this deal. Nigerian regulators have delayed or blocked fintech transactions before. The December 2026 deadline is a target, not a certainty.

2. MoMo PSB is still playing catch-up

OPay and PalmPay have built deep roots in Nigeria’s agent banking space. MoMo PSB has MTN’s brand behind it, but brand alone doesn’t win mobile money wars. Execution does.

3. Restructuring doesn’t fix product problems

If MoMo’s app crashes or agents run out of cash, a new ownership structure won’t fix that immediately. The operational improvements need to follow the financial restructuring.

4. MTN Nigeria’s 40% stake is still meaningful

MTN Nigeria isn’t exiting fintech. It keeps 40%. But it also means MTN Nigeria still has some exposure if MoMo PSB continues to underperform.

5. The unbanked population needs more than apps

Millions of Nigerians who use MoMo PSB are unbanked. They often rely on agents, not smartphones. Any improvement strategy must reach those users — not just urban smartphone users.

If you’re interested in how digital financial tools are evolving across Africa, exploring innovation in tech and fintech gives useful broader context.

How This Fits Into Africa’s Bigger Fintech Story

The MTN Nigeria MoMo PSB stake sale 2026 isn’t happening in isolation. Across Africa, telecom companies are rethinking how they run fintech.

Safaricom’s M-Pesa in Kenya is the gold standard. It works because it has dedicated infrastructure, a massive agent network, and years of trust. MTN Group wants to build something similar — but across multiple African countries at once.

By centralising fintech under one holding structure, MTN Group can:

- Share technology across markets (Nigeria, Ghana, Uganda, etc.)

- Attract external investors into the Fintech HoldCo

- Reduce duplication of costs across subsidiaries

- Build a stronger case for a future fintech IPO

That last point is significant. A centralised, well-capitalised fintech arm is easier to list on a stock exchange than scattered subsidiaries. MTN Group may be setting up MoMo for a public listing in the future.

For Nigeria specifically, this could mean more structured investment in MoMo PSB — if MTN Group delivers on its Ambition 2030 promises.

You might also find it useful to check out featured fintech and tech business stories for more context on how these deals reshape markets.

What Should You Watch For Next?

Here’s what to track over the rest of 2026:

| Milestone | What to Watch |

|---|---|

| CBN Regulatory Approval | Will it come before December 2026? |

| Fintech HoldCo Registration | When is it officially registered? |

| MoMo PSB Service Changes | Any new features or agent expansion? |

| MTN Nigeria Financial Results | Does the restructuring ease balance sheet pressure? |

| Competitor Response | How do OPay, PalmPay react? |

So here’s a question worth sitting with: If MoMo PSB gets the capital and strategy it needs, can it realistically challenge OPay’s dominance in Nigeria? That answer will define whether this deal was worth it.

For broader reading on how tech companies restructure and compete, trending tech business stories are worth bookmarking.

Conclusion: A Big Move With Real Potential — But Patience Required

The MTN Nigeria MoMo PSB stake sale 2026 is one of the most significant fintech deals in Nigeria this year. It’s not just about money changing hands. It’s about MTN Group taking direct control of its African fintech future.

For MTN Nigeria, the deal brings relief. It reduces the financial burden of running a loss-making fintech unit. For MoMo PSB users, it brings the possibility of better service — but only if the restructuring leads to real operational improvements.

Here’s what you can do right now:

- ✅ Keep using MoMo PSB — nothing changes for users until regulatory approval

- ✅ Watch the CBN’s decision — that’s the real turning point

- ✅ Compare your options — OPay, PalmPay, Kuda, and Moniepoint are all active alternatives

- ✅ Stay informed — follow the latest in tech and fintech news to track this deal’s progress

This deal is a bet on Nigeria’s fintech future. Whether it pays off depends on execution, regulation, and competition. The foundation is being laid — what gets built on it is the real story to watch.

About Tech Embed

Tech Embed is a Nigeria-focused tech media platform covering startups, apps, fintech, digital trends, and innovation across Africa. We break down complex tech stories into clear, practical insights that actually make sense. From product launches to industry shifts, our goal is simple — help you understand how technology affects your daily life and business.

Source notes can be added in the editorial fields for this story.

No comments